Tuesday☕️

Trending:

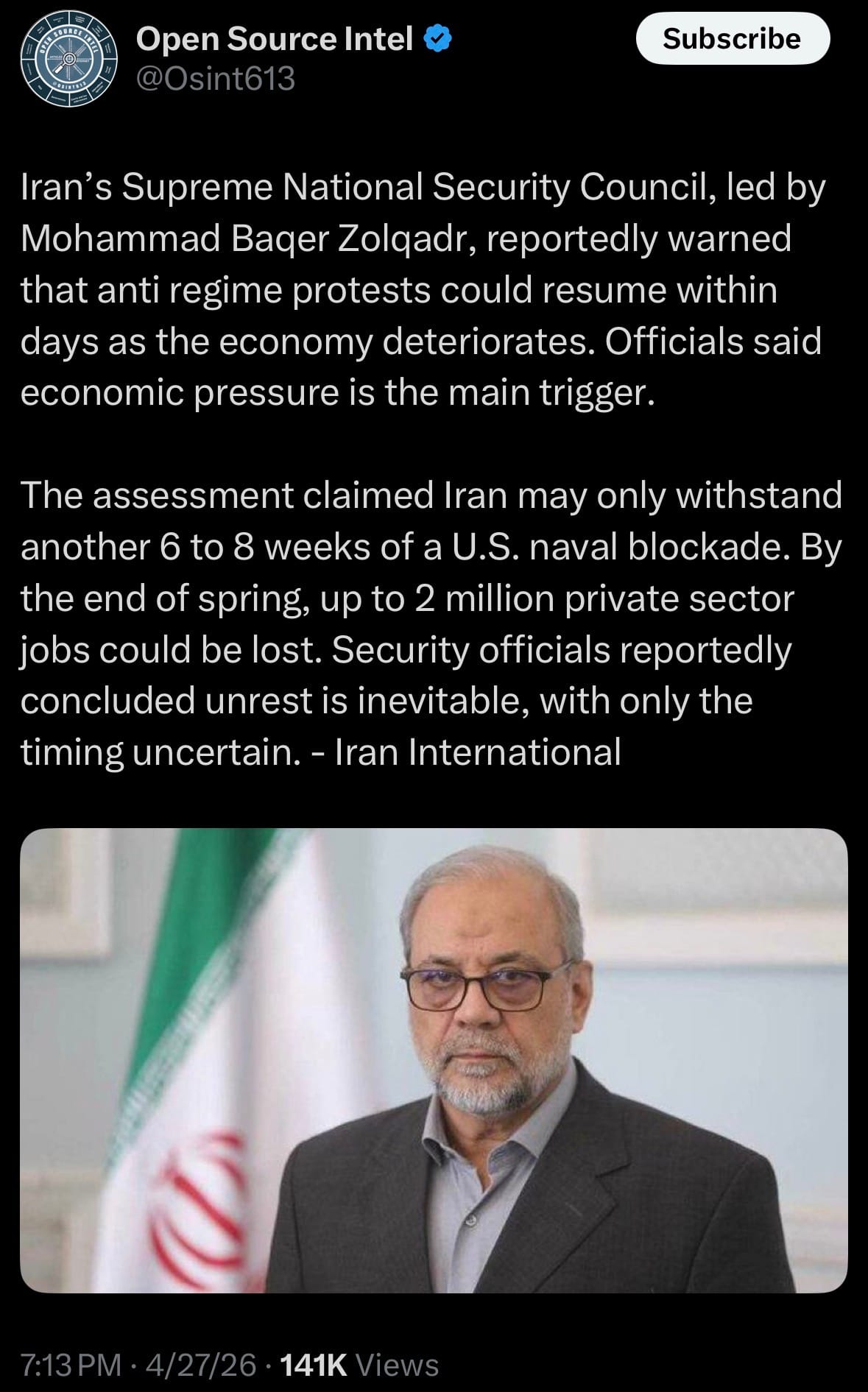

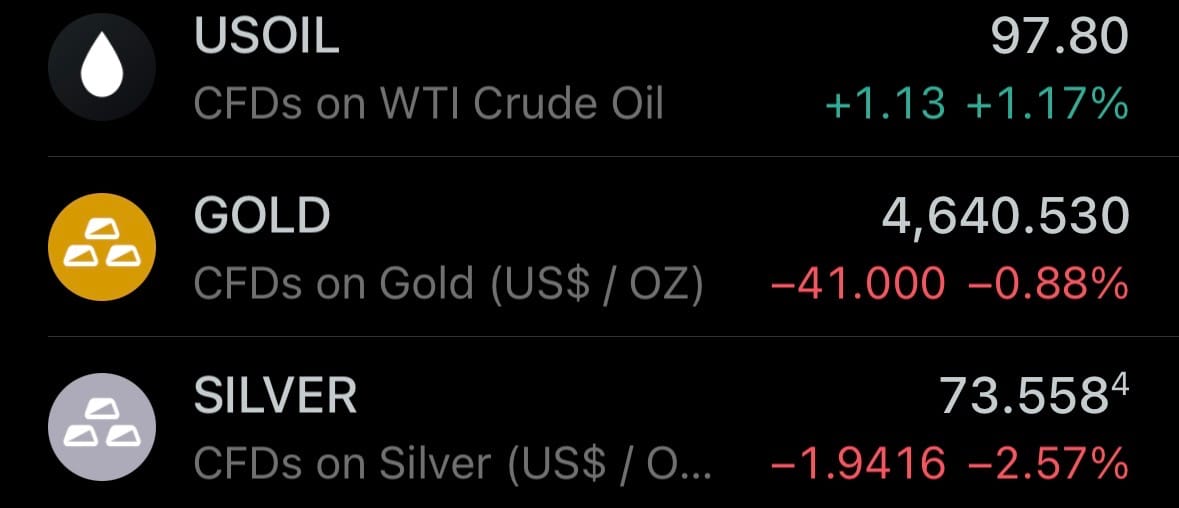

- As of April 28, 2026, Iran’s Supreme National Security Council warned that anti-regime protests could resume within days as the ongoing U.S. naval blockade pushes the economy toward collapse, with officials estimating Iran can only withstand another 6–8 weeks before facing up to 2 million private-sector job losses and inevitable unrest, even as the fragile ceasefire and dual blockade of the Strait of Hormuz remain in effect.

Economics & Markets:

Cyber:

Environment & Weather:

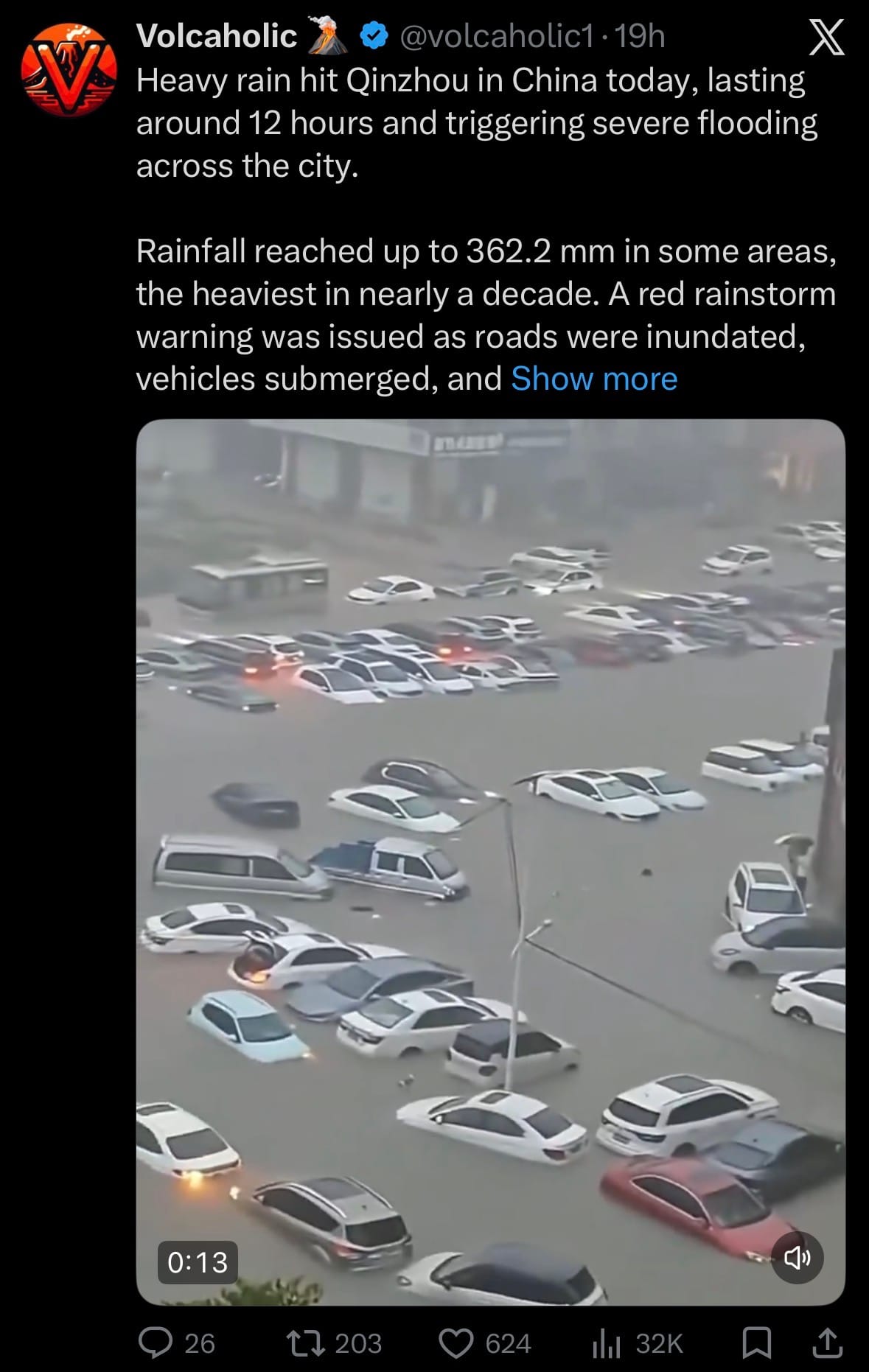

- Over the past 24 hours, Qinzhou in southern China was struck by extreme heavy rainfall of up to 362.2 mm in 12 hours — the heaviest in nearly a decade — triggering severe flooding that submerged roads, vehicles, and buildings while prompting a red rainstorm warning, school suspensions, and orders for residents to stay indoors.

Science & Technology:

Space:

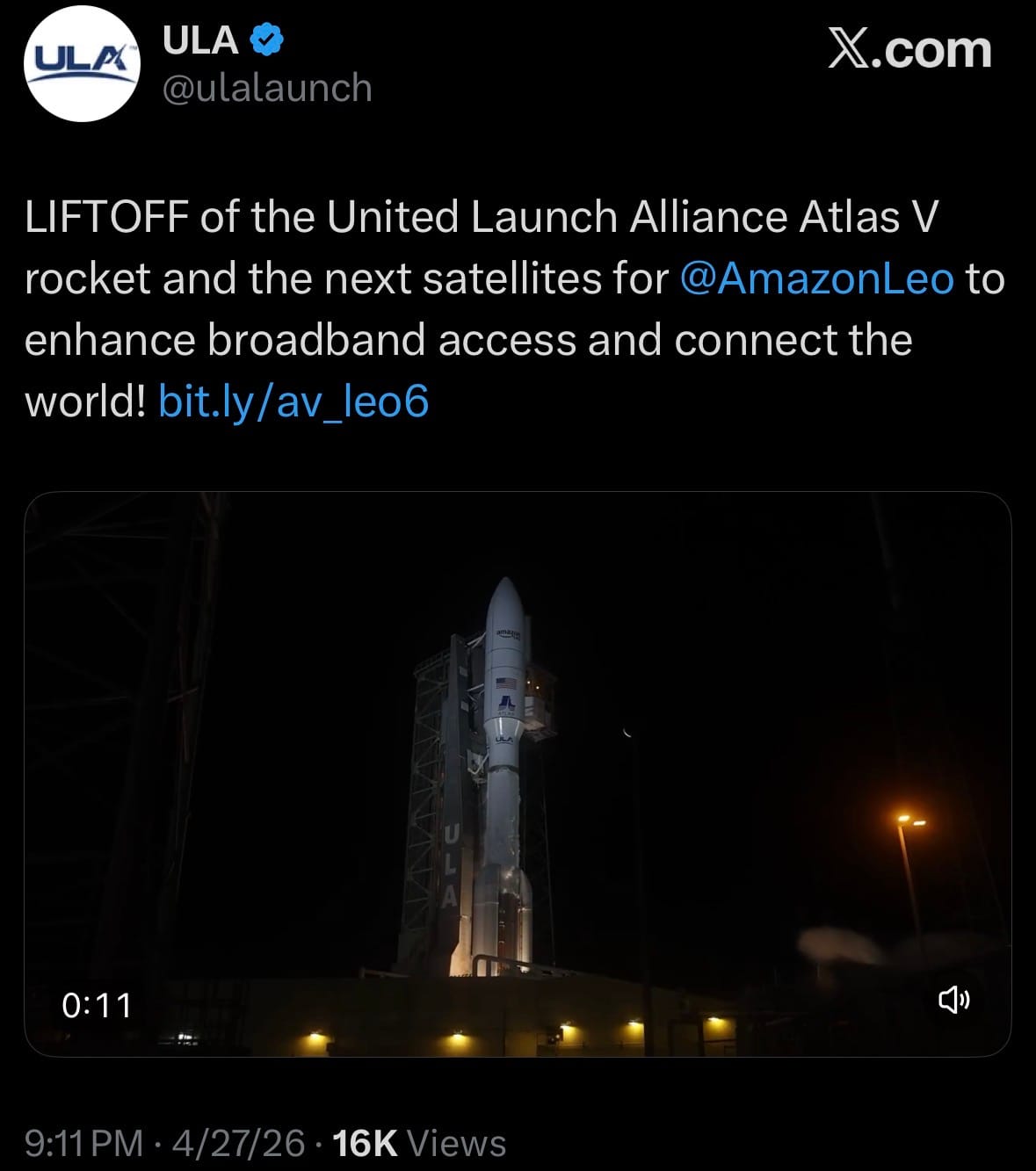

- On April 27/28, 2026, United Launch Alliance successfully launched Amazon Leo (LA-06) on an Atlas V 551 rocket from Cape Canaveral, deploying 29 Amazon Leo satellites into low-Earth orbit and bringing the total constellation to 270 satellites as part of Amazon’s push to build out its global broadband network.

Statistic:

- Largest public hotel companies by market capitalization:

- 🇺🇸 Marriott International: $95.57B

- 🇺🇸 Hilton Worldwide: $76.22B

- 🇺🇸 Las Vegas Sands: $36.09B

- 🇯🇵 Oriental Land: $24.90B

- 🇬🇧 InterContinental Hotels Group: $21.48B

- 🇭🇰 Galaxy Entertainment: $18.32B

- 🇺🇸 Hyatt Hotels: $15.48B

- 🇨🇳 H World Group: $15.33B

- 🇺🇸 Host Hotels & Resorts: $14.35B

- 🇫🇷 Accor: $11.80B

- 🇺🇸 Wynn Resorts: $11.00B

- 🇺🇸 MGM Resorts: $10.37B

- 🇮🇳 Indian Hotels Company: $9.73B

- 🇸🇬 Genting Singapore: $6.69B

- 🇺🇸 Ryman Hospitality Properties: $6.42B

- 🇺🇸 Wyndham Hotels & Resorts: $6.41B

- 🇬🇧 Whitbread: $5.58B

- 🇺🇸 Choice Hotels: $5.44B

- 🇲🇴 MGM China: $5.39B

- 🇨🇳 Atour Lifestyle: $5.09B

- 🇫🇷 Covivio Hotels: $4.35B

- 🇺🇸 Vail Resorts: $4.29B

- 🇭🇰 Mandarin Oriental: $4.22B

- 🇮🇱 Fattal Holdings: $4.06B

- 🇺🇸 Hilton Grand Vacations: $3.77B

History:

- The Federal Reserve was created to solve a structural weakness in the U.S. financial system that existed after the collapse of earlier central banks like the Second Bank of the United States (ended 1836). For nearly 80 years, the U.S. had no central authority to stabilize banking, leading to repeated crises—most notably the Panics of 1873, 1893, and 1907. The Panic of 1907 was decisive: the financial system froze, banks failed, and private banker J.P. Morgan had to personally coordinate bailouts, proving the country lacked an institutional backstop. This led to the Federal Reserve Act (December 23, 1913), creating a hybrid system: a central Board of Governors in Washington and 12 regional Federal Reserve Banks to balance national control with regional economic representation. Its core tools were the ability to issue currency (Federal Reserve Notes), set reserve requirements, lend to banks, and influence credit conditions. Early missteps defined its evolution—during the Great Depression (1929–1930s), the Fed allowed the money supply to collapse by roughly one-third, contributing to widespread bank failures and economic devastation. This failure triggered major reforms under FDR, including the Banking Act of 1935, which strengthened central control, and the creation of the FDIC to prevent bank runs. The 1951 Fed–Treasury Accord was another turning point, giving the Fed independence from direct government financing, allowing it to focus on inflation and economic stability rather than just funding federal debt.

- From the 1970s onward, the Fed became the central engine of economic control. Faced with stagflation, Paul Volcker (1979–1987) raised interest rates above 15%, triggering a deep recession but breaking inflation—establishing credibility that the Fed would prioritize price stability. Under Alan Greenspan (1987–2006), the Fed evolved into a market stabilizer, stepping in during crises like the 1987 crash, LTCM collapse (1998), and dot-com bust (2000), creating what many called the “Fed put”—the expectation it would intervene to support markets. This role expanded massively during the 2008 financial crisis, when the Fed cut rates to near zero and introduced quantitative easing (QE)—buying Treasury bonds and mortgage-backed securities at scale, expanding its balance sheet from under $1 trillion to over $4 trillion. This marked a permanent shift: the Fed became not just a regulator of money, but a direct participant in financial markets. During COVID-19 (2020–2022), this power accelerated—rates dropped to zero again, and the Fed expanded its balance sheet to nearly $9 trillion, while also supporting corporate bond markets and emergency lending programs. Over the past 3 years (2023–2026), the Fed has been navigating one of its most difficult environments: post-pandemic inflation surged to levels not seen in decades (peaking around 9% in 2022), forcing the Fed into one of the fastest rate-hiking cycles in history through 2022–2023, rapidly increasing rates above 5%. This triggered stress in the banking system, including the regional bank failures in 2023 (e.g., Silicon Valley Bank), forcing the Fed to balance inflation control with financial stability. By 2024–2026, the Fed has been managing a tightrope: keeping rates elevated to control inflation while signaling potential easing to avoid recession, all while reducing its balance sheet through quantitative tightening (QT). At the same time, it is exploring future systems like central bank digital currency (CBDC) frameworks, real-time payment rails (FedNow launched 2023), and deeper integration with global financial stability efforts. Today, the Federal Reserve is effectively the core operating system of the global financial order, controlling the world’s reserve currency, influencing global liquidity, and shaping everything from mortgage rates to international capital flows—its decisions now ripple instantly across every major economy on Earth.

Image of the day:

Thanks for reading! Earth is complicated, we make it simple.

- Download our mobile app:

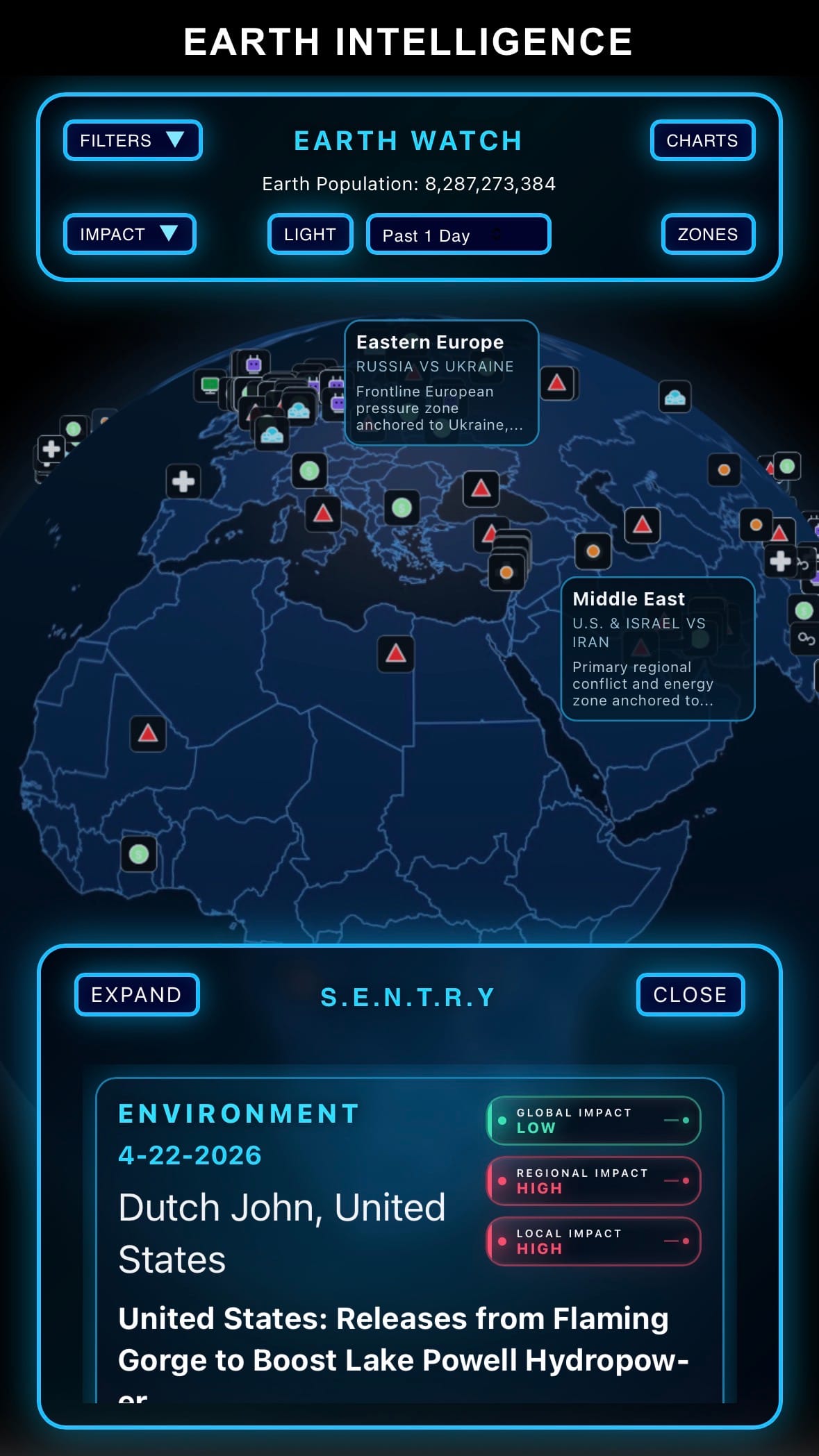

- Click below if you’d like to view our free EARTH WATCH globe:

Click below to view our previous newsletters:

Support/Suggestions Email:

support@earthintel.io