Wednesday☕️

Trending:

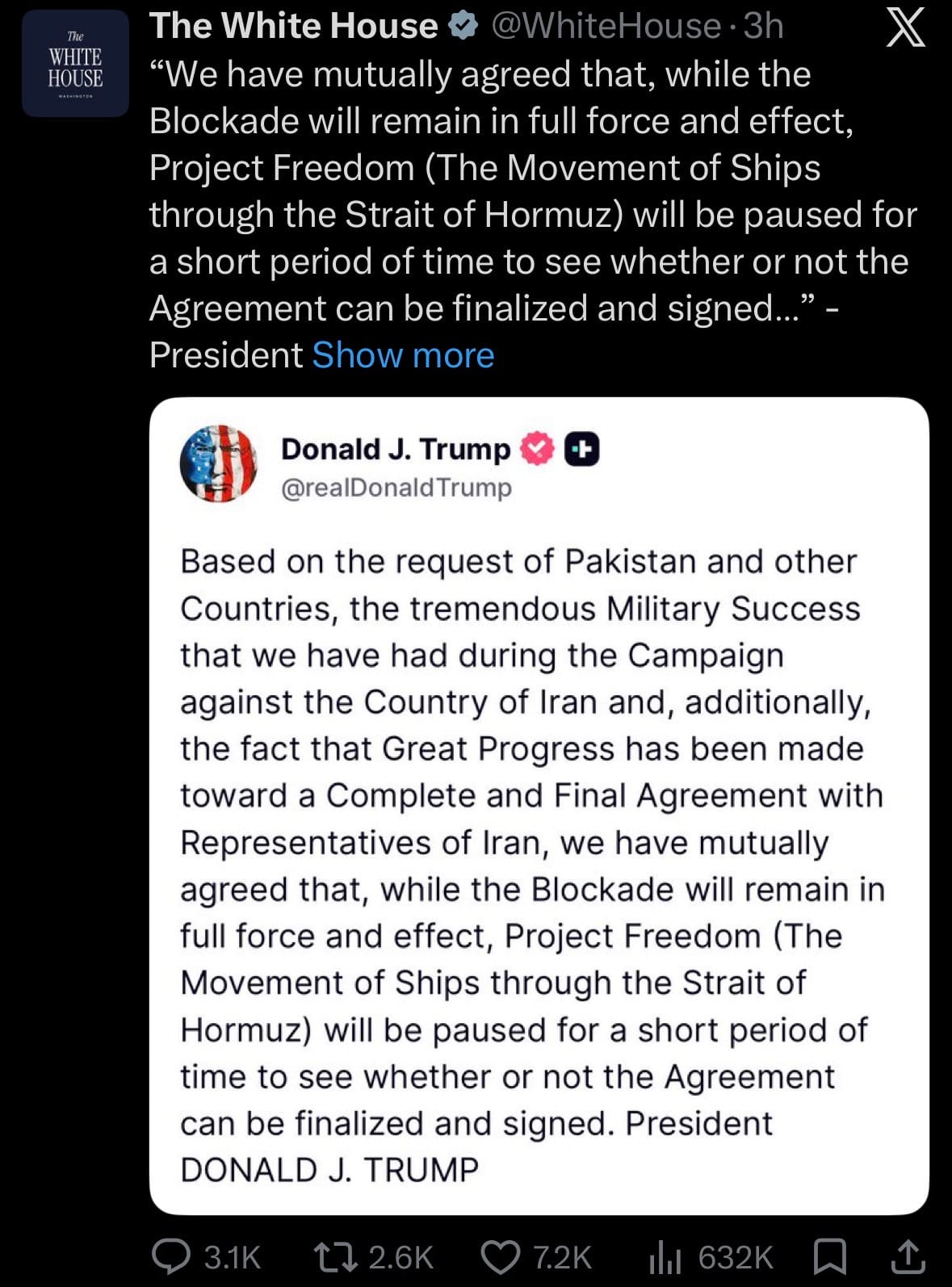

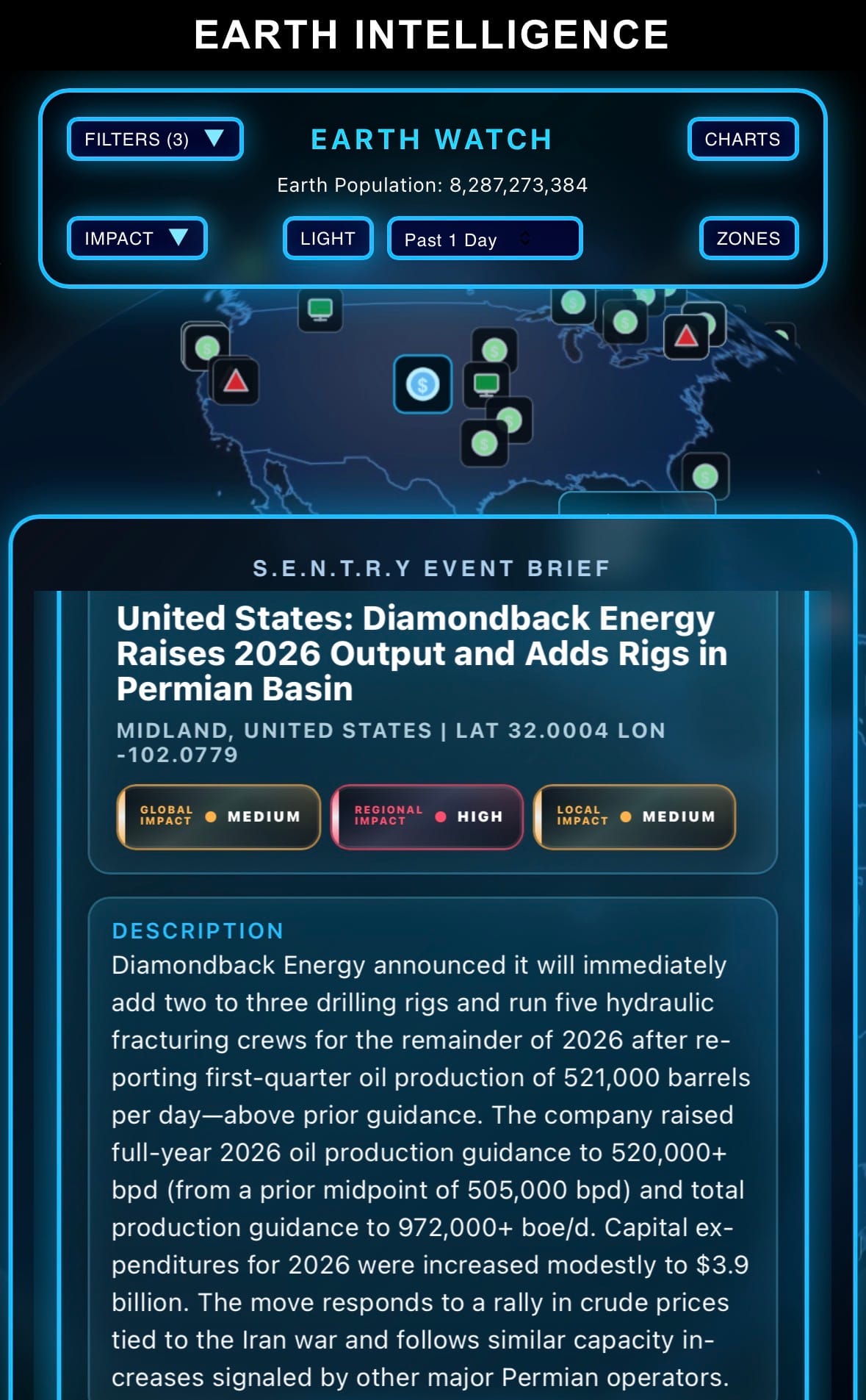

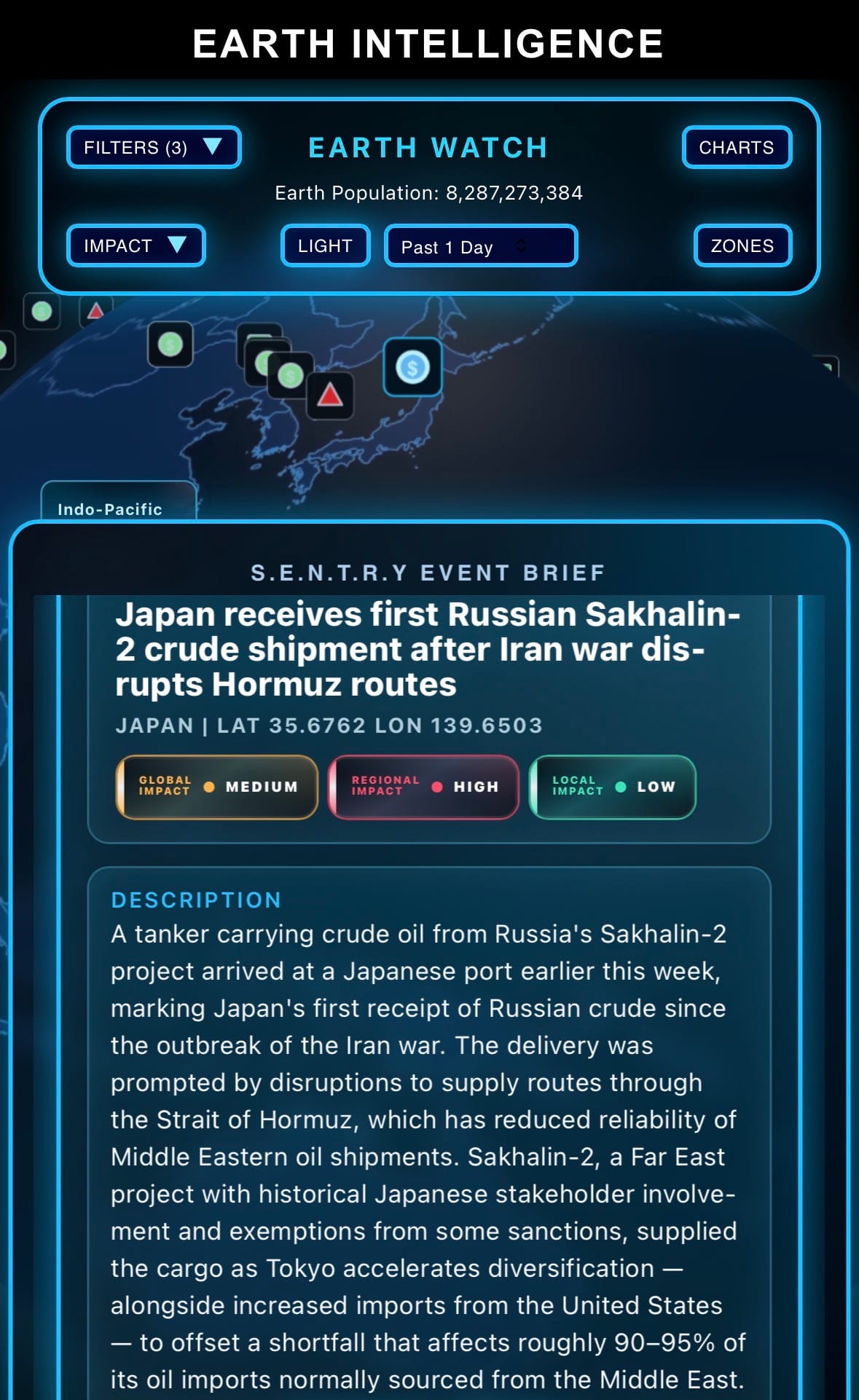

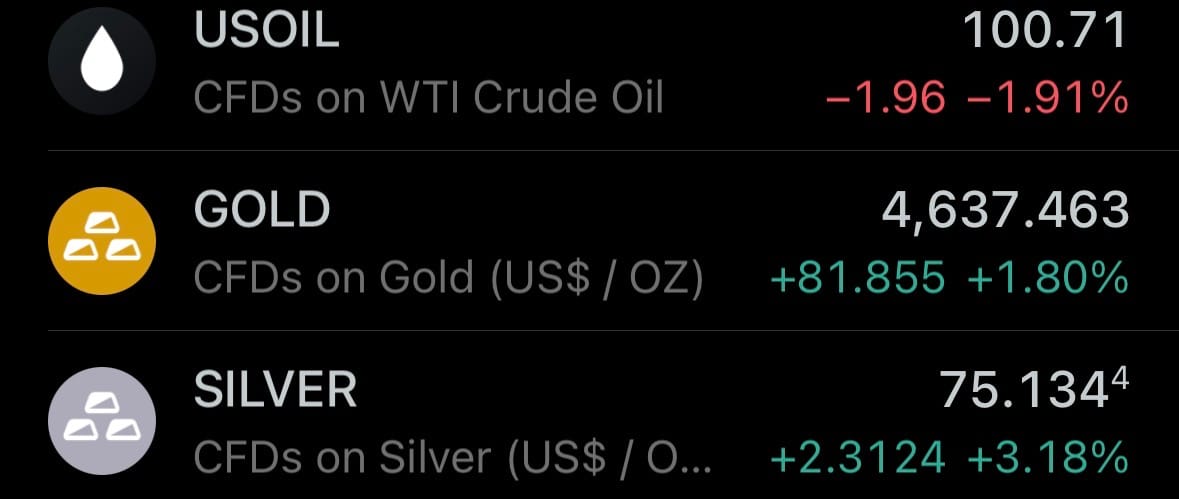

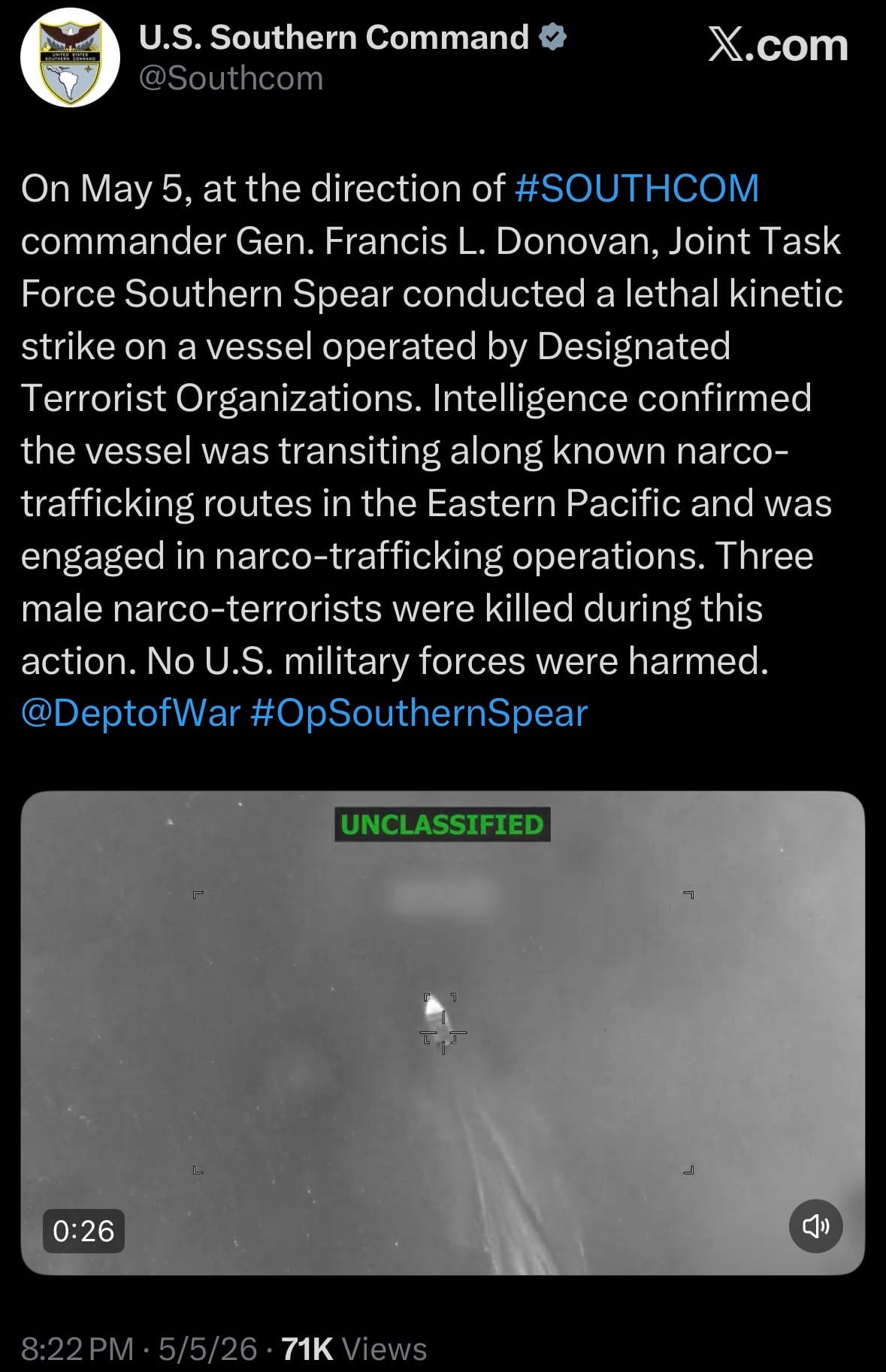

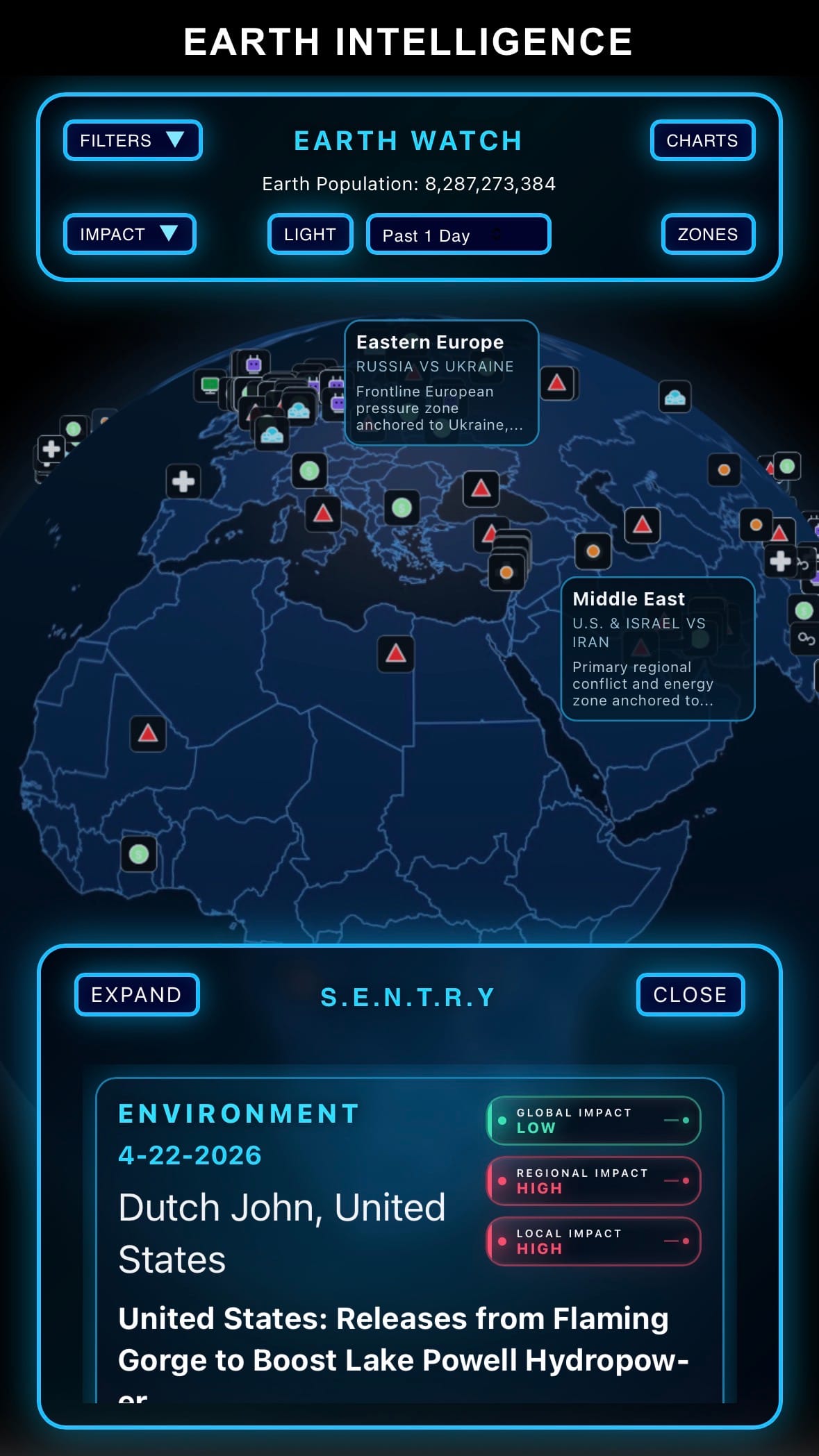

- The U.S. has agreed to temporarily pause Project Freedom — the military escort operation protecting commercial ships through the Strait of Hormuz — for a short time. However, the naval blockade stays fully active — no Iranian tankers or military vessels can move freely.

Economics & Markets:

Geopolitics & Military Activity:

Cyber:

Science & Technology:

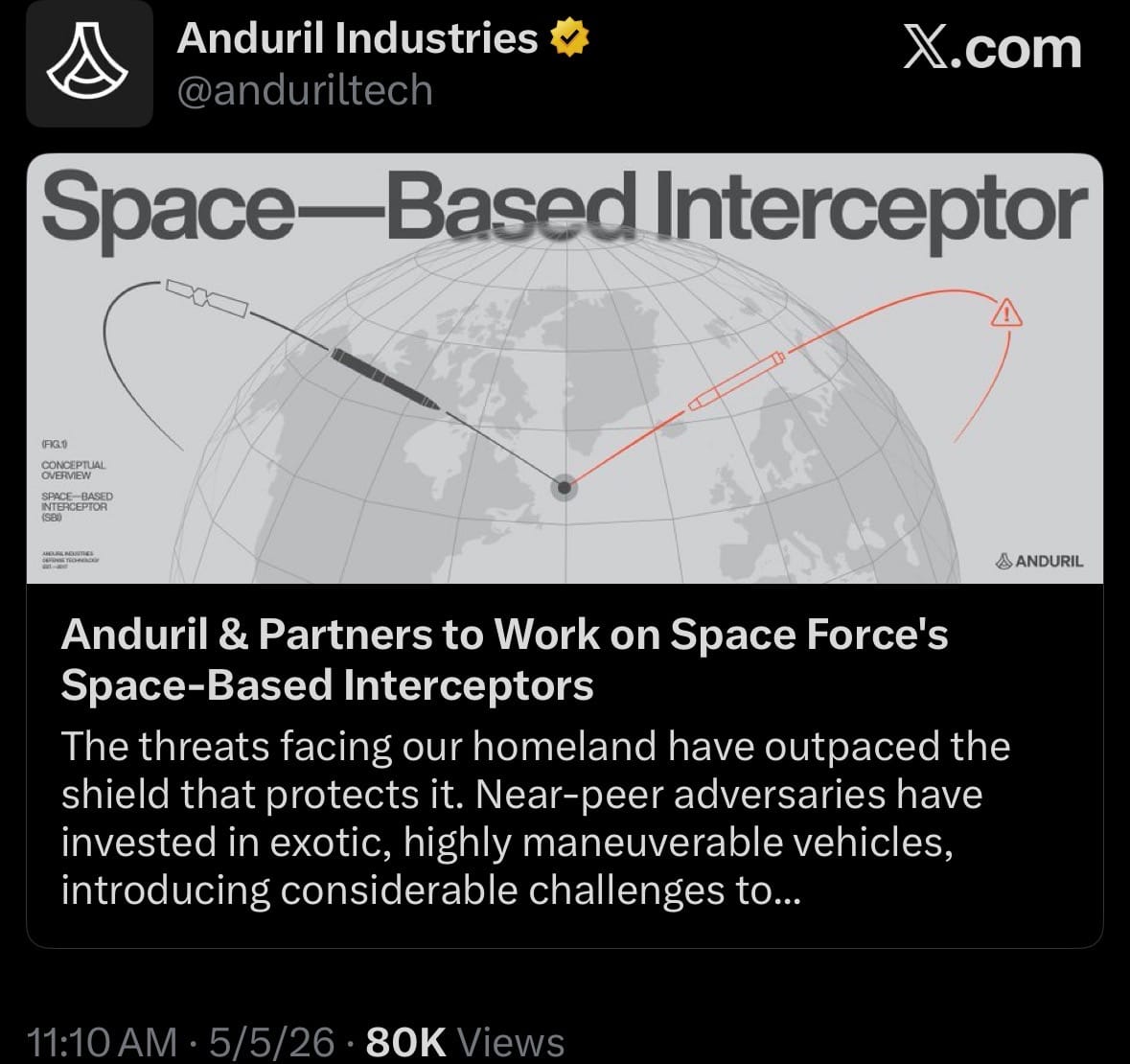

- Anduril is leading a team of defense and space companies to develop and deliver Space-Based Interceptors (SBIs) as part of the Department of War’s Golden Dome for America initiative. These interceptors are satellites placed in orbit that can rapidly destroy incoming enemy ballistic missiles from space.

- They hunt and physically collide with (or explode near) hostile missiles during their boost or midcourse phase — essentially knocking them down before they can reach the United States or its allies. This creates a layered homeland defense system that is fast, scalable, and hard for adversaries to overwhelm.

Statistic:

- Largest banking companies on Earth by market capitalization:

- 🇺🇸 JPMorgan Chase: $829.04B

- 🇨🇳 China Construction Bank: $377.26B

- 🇺🇸 Bank of America: $376.97B

- 🇨🇳 Agricultural Bank of China: $349.97B

- 🇨🇳 ICBC: $316.54B

- 🇺🇸 Morgan Stanley: $300.50B

- 🇬🇧 HSBC: $299.75B

- 🇺🇸 Goldman Sachs: $271.07B

- 🇨🇳 Bank of China: $267.95B

- 🇨🇦 Royal Bank of Canada: $248.17B

- 🇺🇸 Wells Fargo: $244.47B

- 🇺🇸 Citigroup: $223.93B

- 🇦🇺 Commonwealth Bank: $213.95B

- 🇯🇵 Mitsubishi UFJ Financial: $200.46B

- 🇨🇦 Toronto Dominion Bank: $177.63B

- 🇪🇸 Santander: $171.07B

- 🇺🇸 Charles Schwab: $161.90B

- 🇨🇳 CM Bank: $152.74B

- 🇨🇭 UBS: $136.86B

- 🇯🇵 Sumitomo Mitsui Financial Group: $134.90B

- 🇸🇬 DBS Group: $130.79B

- 🇮🇳 HDFC Bank: $127.42B

- 🇺🇸 Capital One: $120.29B

- 🇪🇸 BBVA: $119.38B

- 🇮🇹 UniCredit: $118.91B

History:

- The history of batteries, lithium, and charging networks is really the history of who controls modern energy storage—the foundation of everything from smartphones and laptops to electric vehicles, drones, satellites, and future military systems. Batteries began in the late 1700s, when Alessandro Volta invented the voltaic pile in 1800, creating the first true battery capable of producing continuous electrical current. Through the 1800s, lead-acid batteries (invented 1859 by Gaston Planté) became the first rechargeable systems and were widely used in vehicles and industrial systems. The real transformation came in the 20th century with portable electronics, leading to nickel-cadmium and nickel-metal hydride batteries, but the biggest breakthrough was the development of the lithium-ion battery in the 1970s–1980s, pioneered by scientists like John B. Goodenough, Stanley Whittingham, and Akira Yoshino. Commercialized by Sony in 1991, lithium-ion batteries offered high energy density, rechargeability, and compact size, making them ideal for modern electronics and eventually electric vehicles. As smartphones, laptops, and EVs exploded globally in the 2000s–2020s, lithium became one of the world’s most strategic resources. Major lithium reserves are concentrated in the “Lithium Triangle” (Chile, Argentina, Bolivia) along with Australia and China, but China moved aggressively to dominate not just mining, but the entire supply chain—refining, battery production, and component manufacturing. By the early 2020s, China controlled a majority of global lithium refining capacity and much of the battery materials ecosystem, while companies like CATL and BYD became dominant global battery producers.

- At the same time, charging infrastructure became its own strategic network layer. In the early EV era, charging systems were fragmented, but companies like Tesla transformed the landscape by building the Supercharger network starting in 2012, creating one of the first reliable, high-speed global charging ecosystems integrated directly with vehicles and software. Europe developed large public charging expansions through companies like Ionity, while China massively scaled state-backed charging infrastructure, building one of the world’s largest EV charging networks by the 2020s. Governments increasingly recognized batteries and charging systems as strategic infrastructure, similar to oil pipelines or railroads in previous eras. The U.S. began pushing supply chain independence through laws like the Inflation Reduction Act (2022), incentivizing domestic battery manufacturing and mineral sourcing to reduce reliance on China. By 2023–2026, competition intensified around not just lithium, but also nickel, cobalt, graphite, rare earths, and next-generation battery chemistries like solid-state batteries and sodium-ion systems. Charging networks also became battlegrounds for standards and control—Tesla’s charging connector (NACS) was adopted by many automakers in North America by 2024–2025, giving Tesla major influence over future EV infrastructure. Today, control over batteries, lithium supply chains, and charging networks is effectively a new form of industrial and geopolitical power: whoever controls energy storage and distribution controls transportation, AI infrastructure, defense systems, and the next generation of electrified economies.

Image of the day:

Thanks for reading! Earth is complicated, we make it simple.

- Download our mobile app:

- Click below if you’d like to view our free EARTH WATCH globe:

Click below to view our previous newsletters:

Support/Suggestions Email:

support@earthintel.io